All Categories

Featured

Table of Contents

The are entire life insurance policy and universal life insurance. grows money worth at an ensured rate of interest and additionally through non-guaranteed returns. expands cash money worth at a fixed or variable rate, depending on the insurer and plan terms. The cash money value is not contributed to the fatality advantage. Money value is a feature you make the most of while alive.

After 10 years, the cash value has actually grown to roughly $150,000. He obtains a tax-free funding of $50,000 to begin a business with his bro. The plan loan interest price is 6%. He settles the lending over the next 5 years. Going this course, the rate of interest he pays goes back into his policy's money worth as opposed to an economic institution.

Think of never having to fret regarding bank lendings or high rate of interest prices again. That's the power of unlimited banking life insurance policy.

There's no set funding term, and you have the flexibility to choose the settlement routine, which can be as leisurely as repaying the funding at the time of fatality. This versatility includes the servicing of the loans, where you can decide for interest-only settlements, maintaining the finance balance level and manageable.

Holding cash in an IUL dealt with account being credited passion can frequently be better than holding the cash money on deposit at a bank.: You've constantly desired for opening your own bakeshop. You can borrow from your IUL plan to cover the initial costs of leasing a space, purchasing tools, and hiring personnel.

Infinite Banking 101

Personal lendings can be acquired from typical banks and credit score unions. Right here are some bottom lines to think about. Credit history cards can provide a versatile method to obtain money for really temporary durations. Obtaining money on a credit history card is usually extremely pricey with annual portion prices of passion (APR) usually reaching 20% to 30% or even more a year.

The tax therapy of plan lendings can vary significantly depending upon your nation of house and the particular terms of your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan lendings are normally tax-free, providing a significant benefit. However, in various other territories, there may be tax ramifications to consider, such as potential taxes on the financing.

Term life insurance just supplies a fatality benefit, without any type of cash worth accumulation. This suggests there's no cash worth to obtain versus. This post is authored by Carlton Crabbe, President of Funding permanently, a specialist in giving indexed global life insurance policy accounts. The info offered in this short article is for instructional and informative purposes just and should not be construed as monetary or investment recommendations.

Infinite Banking Agents

When you initially read about the Infinite Banking Principle (IBC), your very first reaction could be: This seems too good to be real. Possibly you're cynical and think Infinite Financial is a rip-off or scheme - infinite banking concept book. We desire to set the document straight! The trouble with the Infinite Banking Idea is not the idea however those individuals providing an adverse critique of Infinite Financial as a principle.

So as IBC Authorized Practitioners with the Nelson Nash Institute, we assumed we would certainly respond to a few of the top questions people look for online when discovering and recognizing every little thing to do with the Infinite Banking Principle. So, what is Infinite Financial? Infinite Banking was developed by Nelson Nash in 2000 and totally discussed with the publication of his publication Becoming Your Own Lender: Open the Infinite Banking Idea.

Bank Identification Number Visa Infinite

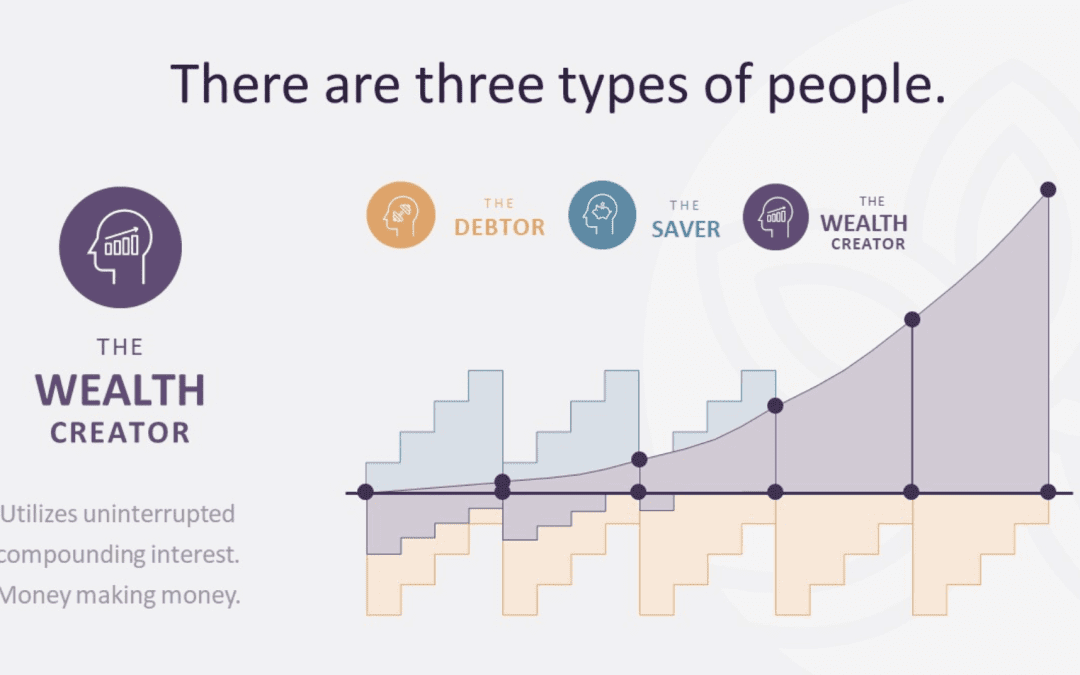

You assume you are coming out monetarily in advance due to the fact that you pay no interest, yet you are not. With conserving and paying cash money, you might not pay passion, however you are utilizing your money once; when you invest it, it's gone forever, and you give up on the opportunity to make lifetime compound passion on that cash.

Billionaires such as Walt Disney, the Rockefeller household and Jim Pattison have actually leveraged the properties of whole life insurance policy that dates back 174 years. Even banks make use of whole life insurance coverage for the same objectives. It is called Bank-Owned-Life-Insurance (BOLI). The Canada Revenue Agency (CRA) even recognizes the value of taking part entire life insurance policy as a special possession course utilized to create lasting equity securely and naturally and give tax benefits outside the extent of conventional investments.

Banking Concepts

It permits you to produce riches by satisfying the banking function in your own life and the capacity to self-finance significant way of life acquisitions and costs without disrupting the compound passion. Among the simplest methods to think of an IBC-type getting involved entire life insurance policy plan is it is similar to paying a mortgage on a home.

With time, this would develop a "consistent compounding" result. You get the picture! When you borrow from your getting involved whole life insurance policy policy, the cash worth proceeds to expand uninterrupted as if you never ever obtained from it in the first place. This is since you are making use of the cash money worth and survivor benefit as security for a lending from the life insurance policy firm or as security from a third-party lender (referred to as collateral borrowing).

That's why it's crucial to work with a Licensed Life Insurance policy Broker licensed in Infinite Banking that frameworks your participating whole life insurance policy policy properly so you can prevent unfavorable tax implications. Infinite Banking as a monetary method is not for everyone. Below are some of the advantages and disadvantages of Infinite Banking you ought to seriously think about in making a decision whether to move on.

Our favored insurance coverage service provider, Equitable Life of Canada, a shared life insurance policy company, specializes in taking part whole life insurance policy policies certain to Infinite Financial. Additionally, in a shared life insurance policy firm, insurance policy holders are considered firm co-owners and get a share of the divisible excess created annually via rewards. We have a selection of providers to select from, such as Canada Life, Manulife and Sunlight Lifedepending on the needs of our customers.

Please additionally download our 5 Top Concerns to Ask A Boundless Banking Representative Before You Work with Them. For even more details about Infinite Financial check out: Disclaimer: The product given in this newsletter is for informational and/or instructional purposes only. The details, viewpoints and/or sights shared in this newsletter are those of the authors and not necessarily those of the supplier.

Banking With Life

Nash was a finance specialist and fan of the Austrian institution of economics, which advocates that the worth of goods aren't clearly the outcome of standard economic structures like supply and need. Instead, people value cash and goods in a different way based on their financial standing and needs.

One of the challenges of traditional financial, according to Nash, was high-interest prices on financings. As well several people, himself consisted of, got right into financial problem due to dependence on financial establishments.

Infinite Banking needs you to possess your monetary future. For ambitious individuals, it can be the finest economic device ever. Here are the advantages of Infinite Financial: Probably the single most valuable aspect of Infinite Financial is that it boosts your capital. You do not need to go through the hoops of a conventional bank to obtain a funding; just request a plan funding from your life insurance policy firm and funds will certainly be offered to you.

Dividend-paying entire life insurance policy is very reduced risk and provides you, the policyholder, a lot of control. The control that Infinite Banking offers can best be grouped right into two categories: tax obligation benefits and property defenses. One of the reasons entire life insurance is optimal for Infinite Banking is exactly how it's taxed.

Entire life insurance policy plans are non-correlated assets. This is why they function so well as the monetary structure of Infinite Financial. No matter of what takes place on the market (stock, realty, or otherwise), your insurance coverage retains its well worth. Way too many individuals are missing this crucial volatility barrier that aids safeguard and grow riches, instead breaking their money into two containers: savings account and financial investments.

Market-based investments expand wealth much faster yet are subjected to market variations, making them naturally dangerous. What if there were a 3rd container that provided safety yet likewise moderate, surefire returns? Entire life insurance policy is that third pail. Not only is the rate of return on your whole life insurance coverage policy ensured, your survivor benefit and costs are additionally assured.

Bank On Yourself Life Insurance

This framework straightens flawlessly with the concepts of the Continuous Wealth Approach. Infinite Banking attract those seeking better economic control. Right here are its main advantages: Liquidity and accessibility: Policy finances offer prompt access to funds without the restrictions of traditional financial institution finances. Tax effectiveness: The money value grows tax-deferred, and plan finances are tax-free, making it a tax-efficient device for constructing riches.

Property security: In lots of states, the money worth of life insurance coverage is protected from lenders, adding an extra layer of financial safety and security. While Infinite Financial has its qualities, it isn't a one-size-fits-all option, and it features substantial drawbacks. Below's why it may not be the very best method: Infinite Banking frequently calls for elaborate policy structuring, which can confuse policyholders.

{kind=link}

Latest Posts

Infinite Bank Statements

Infinite Banking Method

How To Start A Bank: Complete Guide To Launch (2025)